In the complex world of auto accidents, understanding the concept of no fault states is crucial for drivers and insurance policyholders alike. No fault states are jurisdictions where drivers are required to carry personal injury protection (PIP) insurance, which covers medical expenses and other related costs regardless of who was at fault in an accident. This system aims to reduce legal disputes and expedite compensation for injured parties, making it a significant aspect of auto insurance in the United States.

In this article, we will explore what no fault states are, how they operate, and their advantages and disadvantages. We will also provide a comprehensive list of states that follow this system and discuss how it affects drivers and their insurance claims. If you are a driver or someone interested in auto insurance, understanding the nuances of no fault states can help you navigate the complexities of auto accidents more effectively.

As we delve deeper into this topic, we will also highlight essential statistics, legal implications, and tips for ensuring you are adequately protected in a no fault state. With the right knowledge, you can make informed decisions that will safeguard your interests in the event of an auto accident.

Table of Contents

- What is a No Fault State?

- List of No Fault States

- How Does No Fault Insurance Work?

- Advantages and Disadvantages of No Fault Insurance

- Understanding Personal Injury Protection (PIP)

- No Fault vs. Fault States: A Comparison

- Impact of No Fault Insurance on Auto Insurance Premiums

- Conclusion

What is a No Fault State?

A no fault state is a jurisdiction where the law mandates that drivers must carry insurance that covers their own medical expenses and other related costs, irrespective of who caused the accident. This system is designed to simplify the claims process and minimize the need for litigation. In a no fault state, injured parties seek compensation from their own insurance company rather than pursuing a lawsuit against the at-fault driver.

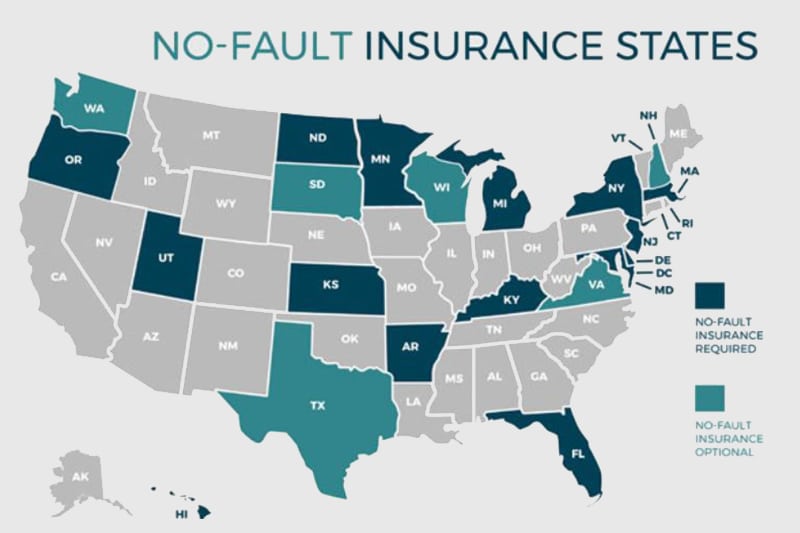

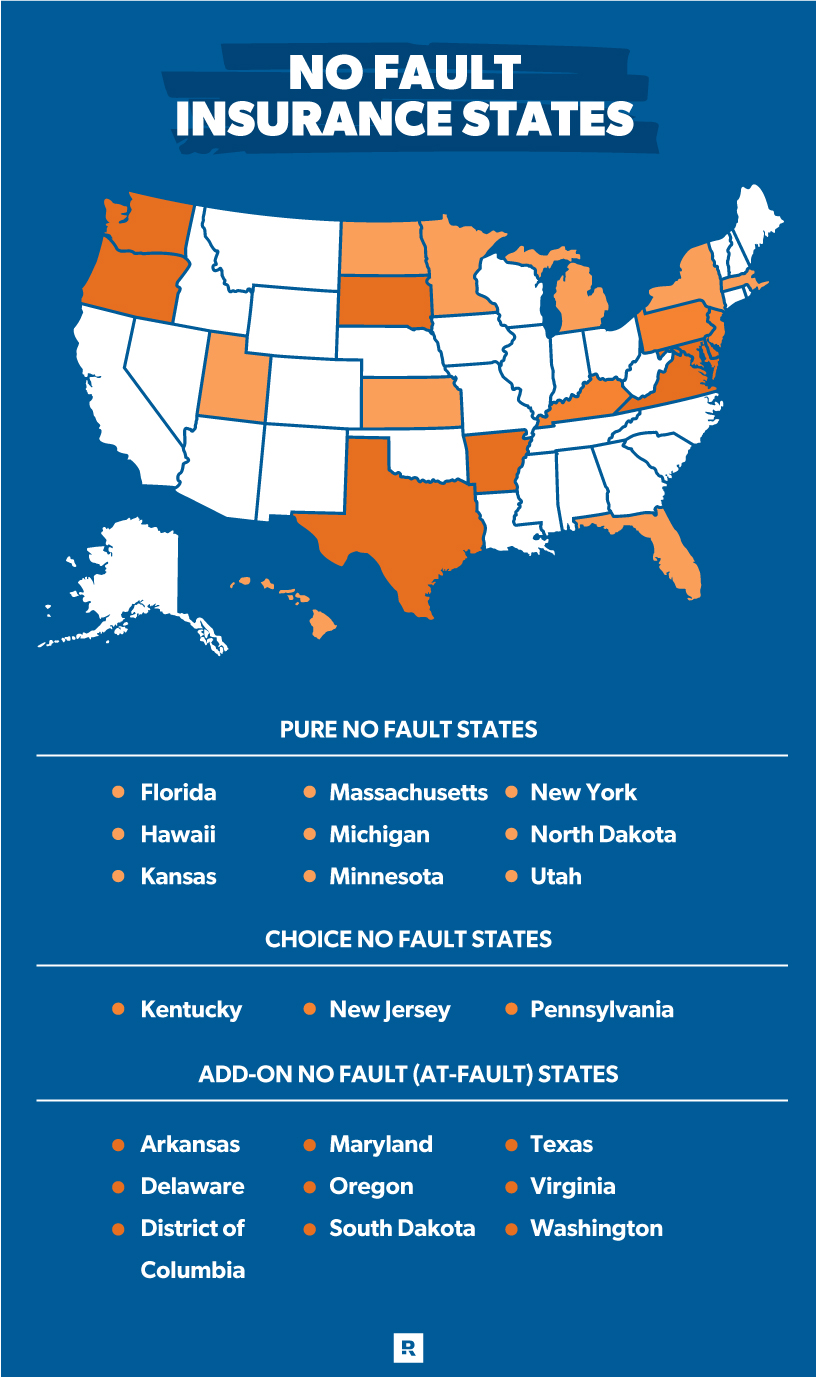

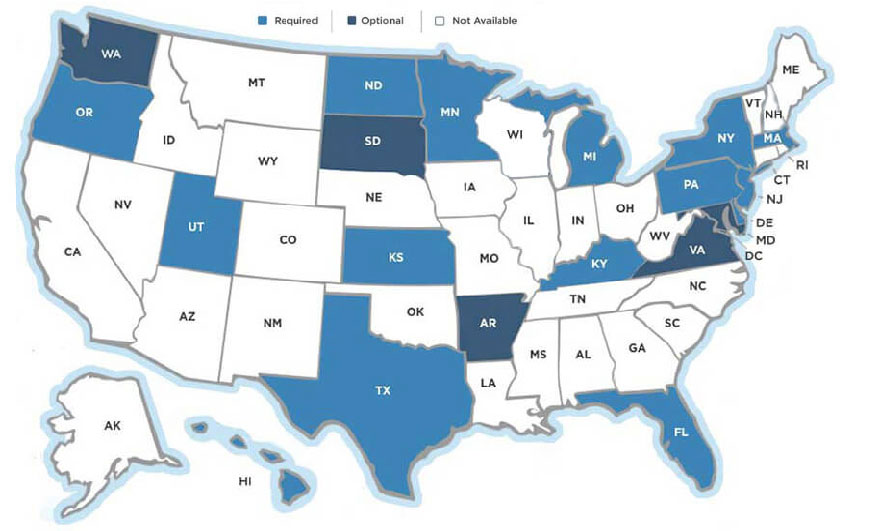

List of No Fault States

As of 2023, the following states operate under a no fault insurance system:

- Florida

- Michigan

- New York

- New Jersey

- Pennsylvania

- Hawaii

- Massachusetts

- North Dakota

- Utah

How Does No Fault Insurance Work?

No fault insurance works by requiring drivers to purchase personal injury protection (PIP) coverage as part of their auto insurance policy. This coverage pays for medical expenses, lost wages, and other necessary costs resulting from an accident, regardless of fault. Here’s how it generally operates:

- When an accident occurs, each party files a claim with their own insurance company.

- The PIP coverage pays for medical bills and other expenses up to the policy limit.

- If the damages exceed the PIP limits or if the injuries are severe, drivers may still have the option to sue the at-fault driver, depending on the state's laws.

Advantages and Disadvantages of No Fault Insurance

Advantages

- Reduces the need for litigation and legal disputes.

- Expedites the claims process, allowing for quicker access to compensation.

- Provides coverage for medical expenses and lost wages regardless of fault.

Disadvantages

- May limit the right to sue for damages, which can be problematic for serious injuries.

- Costs can be higher due to mandatory PIP coverage.

- Some drivers may be underinsured if they rely solely on PIP for serious accidents.

Understanding Personal Injury Protection (PIP)

PIP is a critical component of no fault insurance systems. It covers a variety of expenses, including:

- Medical expenses resulting from injuries sustained in an accident.

- Lost wages due to the inability to work after the accident.

- Other related expenses such as rehabilitation costs and funeral expenses.

Each state has different minimum coverage limits for PIP, so it’s essential to review your policy to ensure you have adequate protection.

No Fault vs. Fault States: A Comparison

In fault states, the driver responsible for the accident is liable for damages and must pay for the other party's medical expenses and property damage. In contrast, no fault states require drivers to seek compensation from their insurance companies, regardless of fault. This fundamental difference impacts how claims are handled and the potential for legal disputes.

Impact of No Fault Insurance on Auto Insurance Premiums

The introduction of no fault insurance can lead to varying effects on auto insurance premiums:

- In some cases, premiums may be lower due to reduced litigation costs.

- However, states with higher medical costs may see increased premiums as PIP coverage requirements rise.

- Drivers in no fault states should regularly review their policies to ensure they are getting the best rates and coverage.

Conclusion

Understanding no fault states and how they operate is essential for all drivers. This system provides a framework that simplifies insurance claims and ensures that injured parties receive compensation swiftly. However, it also presents unique challenges and considerations that drivers must navigate. By being informed about your rights and responsibilities in a no fault state, you can better protect yourself and your financial interests in the event of an auto accident.

We encourage you to leave your thoughts in the comments section below, share this article with friends and family, and explore more insightful content on our website.

Thank You for Reading!

We appreciate your interest in our content and hope you found this article informative. Be sure to visit us again for more articles that can help you navigate the complexities of auto insurance and other important topics.

- Jessica Dube Accident

- Pasta Ramen Menu

- Heather Robinson Tim Robinson

- Hudson County Correctional Facility

- Sam Marrazzo

- Did Kamala Harris Used To Date Montel Williams

- Sophie Rain Spiderman Erome

- Porn Camilla Araujo

- Is Gametimeco Legit

- Whats In A Big Mac