No fault insurance is a unique system of auto insurance that has been adopted by several states in the United States. This insurance model aims to streamline the process of claims and reduce the legal complexities often associated with car accidents. In this article, we will delve into the specifics of no fault insurance, identify which states have adopted this system, and explore its implications for drivers and policyholders.

Understanding no fault insurance is crucial for anyone who drives in the United States, as it affects how claims are handled after an accident. Unlike traditional liability insurance, where the at-fault party is responsible for covering damages, no fault insurance allows drivers to seek compensation from their own insurance providers, regardless of who caused the accident. This can lead to quicker settlements and fewer disputes.

In this comprehensive guide, we will outline the states that currently implement no fault insurance, explain the advantages and disadvantages of this system, and provide insights into how it impacts drivers and their financial responsibilities. Whether you’re a long-time resident or a newcomer to a no fault state, this article will equip you with the knowledge you need to navigate the complexities of auto insurance.

Table of Contents

- What is No Fault Insurance?

- States with No Fault Insurance

- Advantages of No Fault Insurance

- Disadvantages of No Fault Insurance

- How No Fault Insurance Works

- The Impact on Drivers

- Choosing the Right Insurance in No Fault States

- Conclusion

What is No Fault Insurance?

No fault insurance is a type of car insurance that allows drivers to receive compensation for their injuries and damages without having to establish who was at fault for the accident. This system was designed to reduce the burden on courts and minimize the legal disputes that often arise in car accident cases.

In a no fault insurance system, each party involved in an accident submits claims to their own insurance company. This means that regardless of who caused the accident, each driver’s insurance will cover their medical expenses and other damages up to a certain limit defined by their policy.

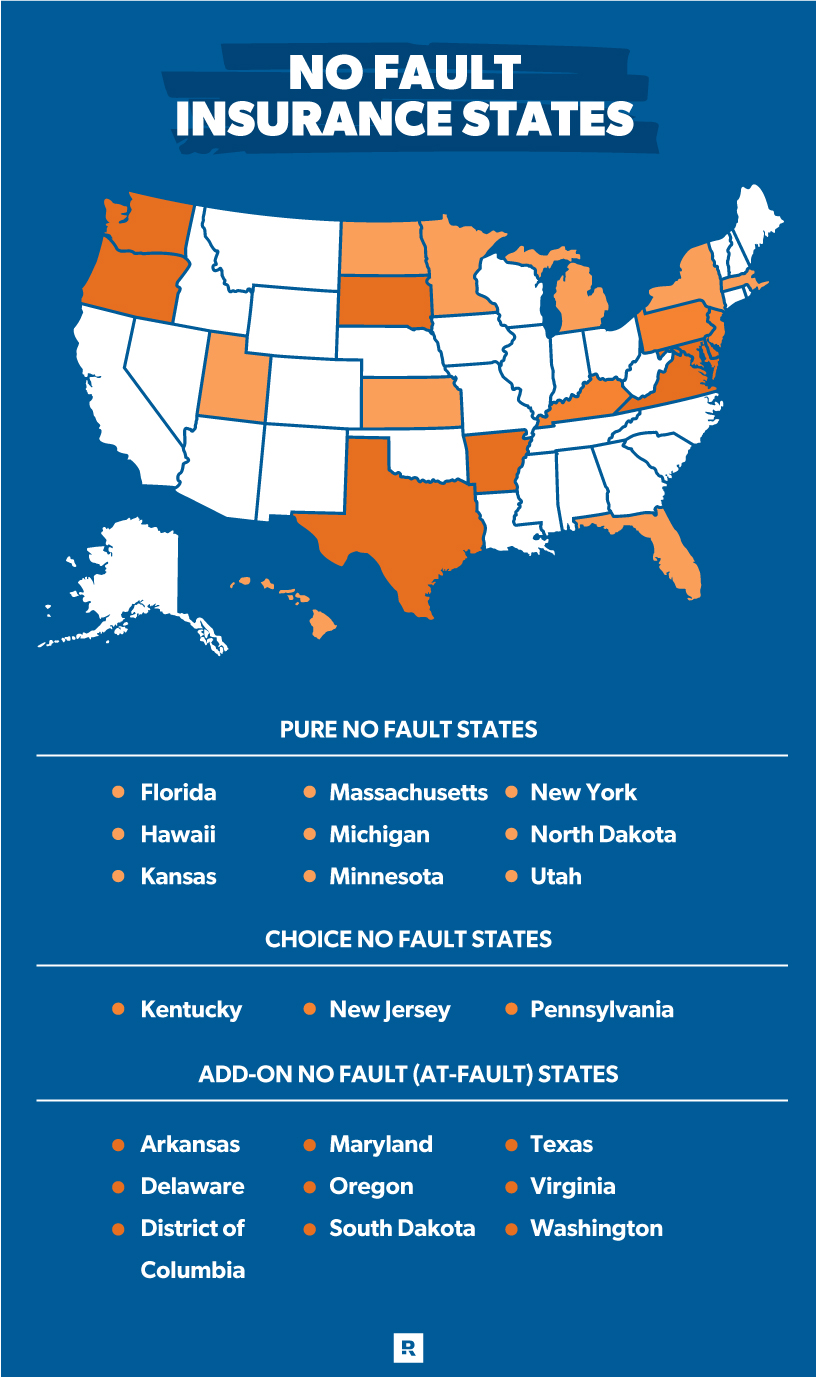

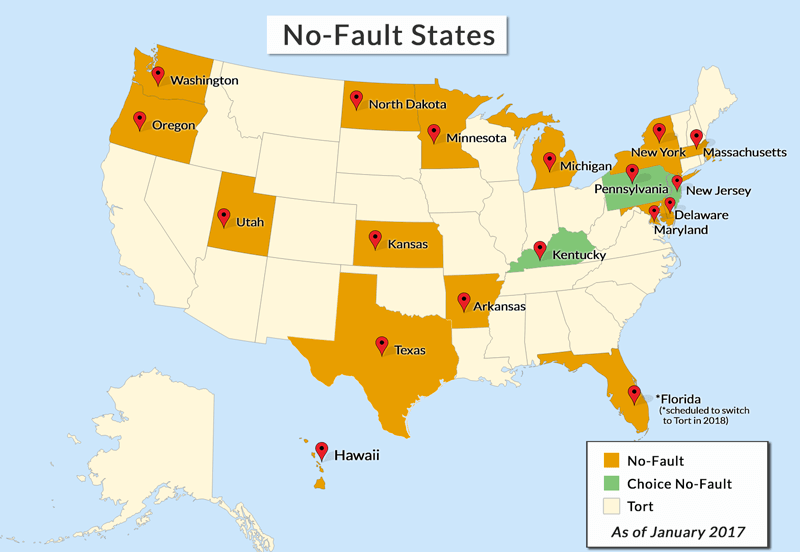

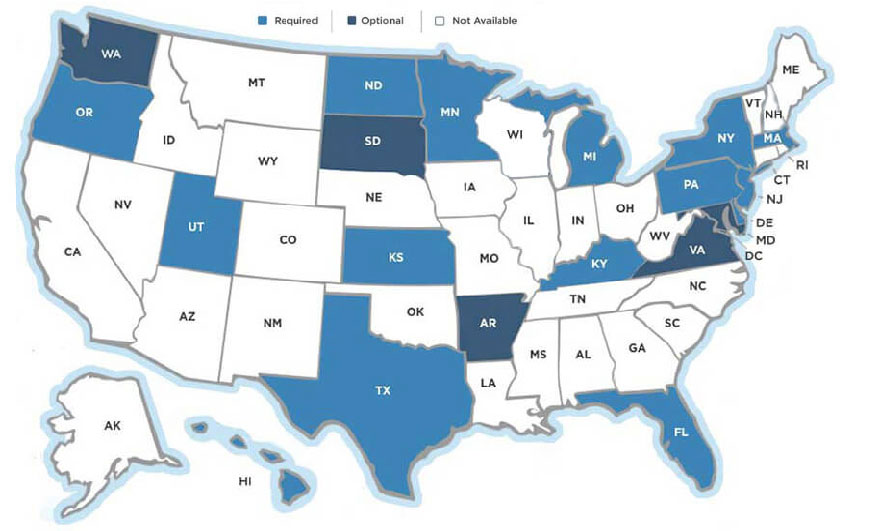

States with No Fault Insurance

As of now, there are a select number of states in the United States that have adopted no fault insurance laws. These states include:

- Florida

- Michigan

- New York

- New Jersey

- Pennsylvania

- Hawaii

- Kentucky

- Massachusetts

- North Dakota

- Utah

Each of these states has its own specific regulations and requirements surrounding no fault insurance, which can vary significantly from one state to another.

Summary of No Fault States

| State | Year Implemented | Key Features |

|---|---|---|

| Florida | 1971 | Personal Injury Protection (PIP) required |

| Michigan | 1973 | Unlimited lifetime benefits for medical expenses |

| New York | 1974 | PIP coverage required; limited right to sue |

| New Jersey | 1972 | Choice of PIP coverage; limited right to sue |

| Pennsylvania | 1984 | Choice between limited and full tort options |

| Hawaii | 1988 | No fault insurance required; PIP coverage |

| Kentucky | 1975 | Mandatory PIP coverage |

| Massachusetts | 1970 | PIP coverage required; limited right to sue |

| North Dakota | 1975 | Mandatory PIP coverage |

| Utah | 1980 | Mandatory PIP coverage |

Advantages of No Fault Insurance

No fault insurance offers several benefits to drivers, which include:

- Faster Claims Processing: Since drivers can claim their own insurance, the claims process is typically faster.

- Reduced Legal Fees: With fewer disputes over fault, drivers may spend less on legal fees.

- Lower Insurance Costs: In some cases, no fault insurance can lead to lower premiums due to reduced litigation costs.

- Guaranteed Coverage: Drivers are assured of receiving compensation for their injuries regardless of fault.

Disadvantages of No Fault Insurance

Despite its advantages, no fault insurance also has its drawbacks:

- Limited Right to Sue: In many no fault states, drivers have limited ability to sue the at-fault driver for damages.

- Higher Premiums: Some drivers may find that premiums are higher than in traditional liability systems.

- Coverage Limitations: No fault insurance policies often have coverage limits, which may not fully cover all expenses.

How No Fault Insurance Works

No fault insurance operates on a straightforward premise: injured parties seek compensation from their own insurance providers. Here’s a basic overview of how it works:

- Accident Occurs: A car accident happens, and both drivers are involved.

- Claim Submission: Each driver submits a claim to their own insurance company.

- Insurance Evaluation: The insurance companies evaluate the claims and determine the benefits payable according to the policy terms.

- Compensation Issued: Each driver receives compensation for their injuries and damages based on their policy limits.

The Impact on Drivers

The no fault insurance system significantly impacts how drivers approach auto insurance. Here are a few key considerations:

- Understanding Policy Options: Drivers need to be well-informed about their policy options and coverage limits.

- Choosing the Right Coverage: Selecting between limited and unlimited coverage can have financial implications.

- Awareness of State Laws: Familiarity with the specific laws in their no fault state is crucial for compliance and protection.

Choosing the Right Insurance in No Fault States

When selecting insurance in a no fault state, drivers should consider the following tips:

- Compare Quotes: Always compare quotes from multiple insurers to find the best rates and coverage options.

- Review Policy Details: Carefully read the policy details, including coverage limits and exclusions.

- Consult with an Expert: Consider speaking to an insurance agent for personalized advice and recommendations.

Conclusion

No fault insurance represents a significant shift in how auto insurance claims are handled in certain states. By understanding the states that implement this system, along with its benefits and drawbacks, drivers can make informed decisions about their auto insurance coverage. We encourage you to leave your comments below, share this article with others, or explore more content on our website to enhance your knowledge about auto insurance.

Thank you for reading, and we look forward to welcoming

- Desirulezco

- Ticket Vs Citation

- Carol Luistro Obituary

- Sam Marrazzo

- Hudson County Correctional Facility

- Shoprite Of West Caldwell

- Sophie Rain Spiderman Erome

- Yololary Onlyfans

- Is Gametimeco Legit

- Heather Robinson Tim Robinson